delta

/ˈdɛltə/

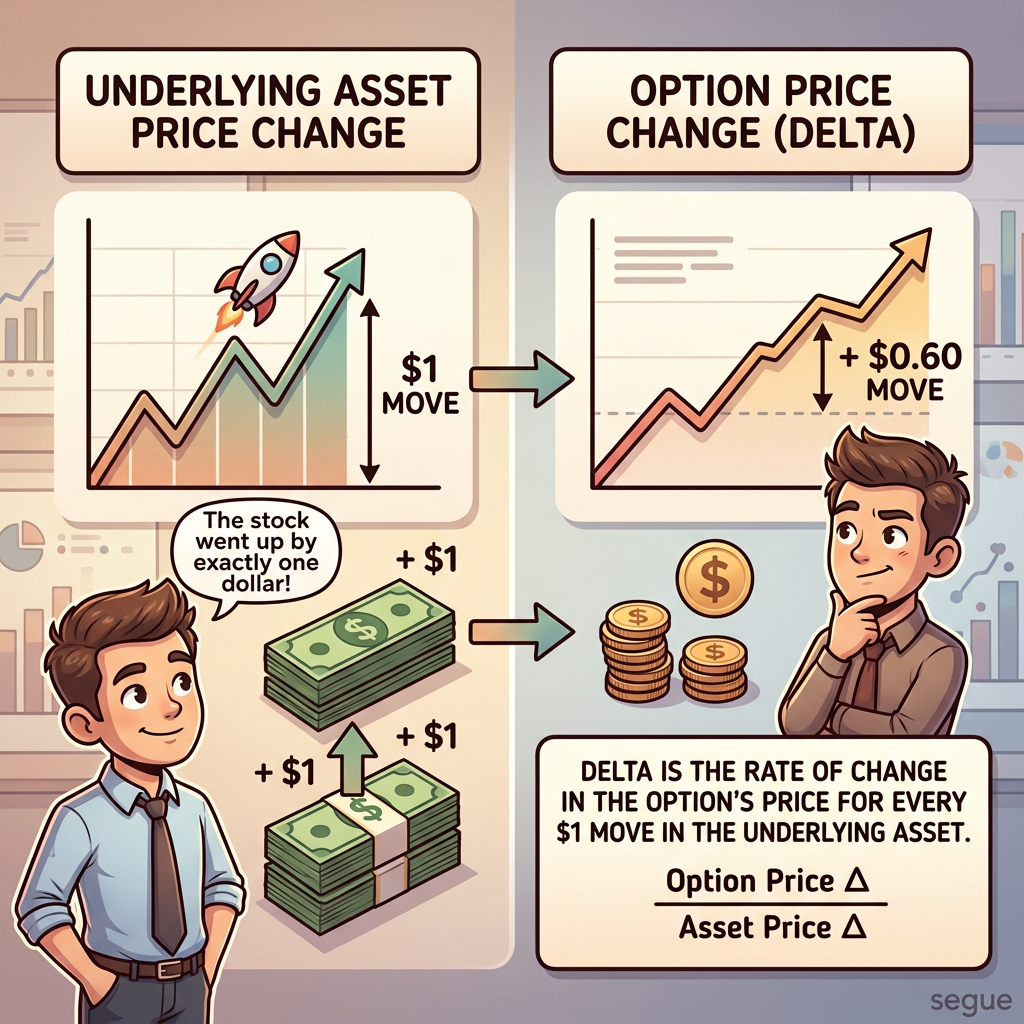

the rate of change in an option's price relative to a $1 move in the underlying asset

delta in a sentence

“The call option had a delta of 0.60, meaning it would gain $0.60 for every $1 the stock rose.”

Origin of delta

Greek letter Δ (delta), used in mathematics to denote change or difference

Related Words

theta

the rate at which an option loses value each day due to the passage of time; time decay

hedge

an investment made to reduce the risk of adverse price movements in an asset

futures contract

an agreement to buy or sell an asset at a predetermined price on a specific future date

leverage

the use of borrowed capital to amplify potential returns — and potential losses

call option

a contract giving the buyer the right, but not obligation, to purchase shares at a set price before expiration

put option

a contract giving the buyer the right, but not obligation, to sell shares at a set price before expiration